EPF — Employee Provident Fund — is one of the most significant financial assets a salaried employee accumulates over a career, and it’s also one of the most undertracked. Contributions happen automatically in the background, deducted from salary each month with a matching employer contribution added on top. Most employees know it exists but couldn’t tell you their current balance, their withdrawal eligibility, or what happens to it when they change jobs.

How EPF actually works

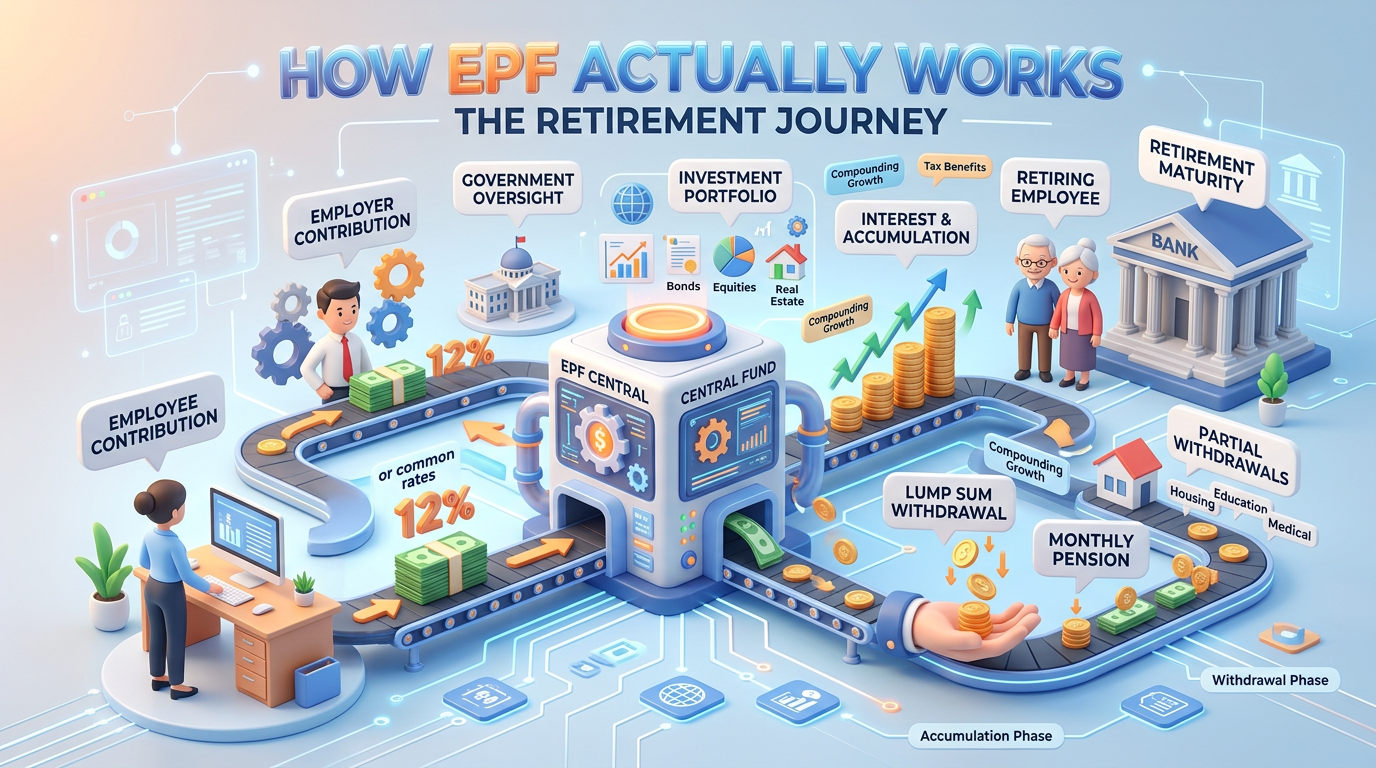

A fixed percentage of a salaried employee’s basic wage is deducted each month and deposited into their EPF account. The employer contributes an additional percentage on top — making EPF effectively a benefit where the employer adds to your retirement savings beyond just your salary. The combined amount grows with a declared interest rate set periodically by the EPFO (Employees’ Provident Fund Organisation).

What makes EPF structurally valuable

- The employer contribution is additional money you receive beyond your salary that goes directly toward long-term savings

- The interest is compounded annually and declared each year

- It has tax advantages at the contribution, accumulation, and (in many cases) withdrawal stages — making it one of the more tax-efficient long-term savings instruments available to salaried employees

What happens when you change jobs

This is where most employees make costly mistakes. EPF can be transferred to a new employer’s account using the UAN (Universal Account Number) — the same UAN follows you across employers. Withdrawing EPF prematurely on a job change forfeits compounded growth and may have tax implications, yet many employees do it simply because they don’t know the transfer process.

Partial withdrawal rules many employees don’t know exist

EPF allows partial withdrawal for specific purposes — housing, medical emergencies, education — under defined conditions. Many employees either didn’t know this exists or assume the entire corpus is inaccessible until retirement.

The passbook most employees have never checked

Every EPF member can check their account balance, contribution history, and employer contribution record through the EPFO portal using their UAN. Most salaried employees have never done this — and some have discrepancies they’re unaware of.

How to Start: Step-by-Step Mini-Guide

- Activate and check your UAN immediately if you haven’t. Your Universal Account Number is the key to tracking and managing all EPF activity — get it from your employer or HR if you don’t have it.

- Log into the EPFO member portal and check your current balance and contribution history. Confirm that employer contributions are appearing correctly — discrepancies happen and need to be flagged early.

- Understand your current employer’s contribution split — not all of the employer’s contribution goes into your EPF; a portion goes into EPS (Employee Pension Scheme), which has different rules.

- If you’ve changed jobs, confirm your EPF was transferred, not withdrawn. Old unclaimed accounts lose track over time — check if you have dormant previous employer accounts.

- Know the partial withdrawal rules relevant to your situation — housing, medical, education eligibility conditions differ and are worth understanding before a need arises.

- Factor your EPF balance into your overall retirement picture. Most people plan retirement savings without accounting for EPF — including it gives a more accurate picture of where you actually stand.

Disclaimer: This content is for educational and informational purposes only and does not constitute financial or legal advice. EPF rules, interest rates, and withdrawal conditions are governed by EPFO regulations which are subject to change — please consult official EPFO resources or a licensed financial advisor for guidance specific to your situation.

Leave a Reply